The vault market is splitting into three. RockSolid is stuck in the middle.

When you look at the numbers long enough, a pattern appears. Not at the protocol level (fund flows, after all, are just ticks on a chart). But at the structure level: how capital moves between risk profiles, and which products catch it at each point in the journey.

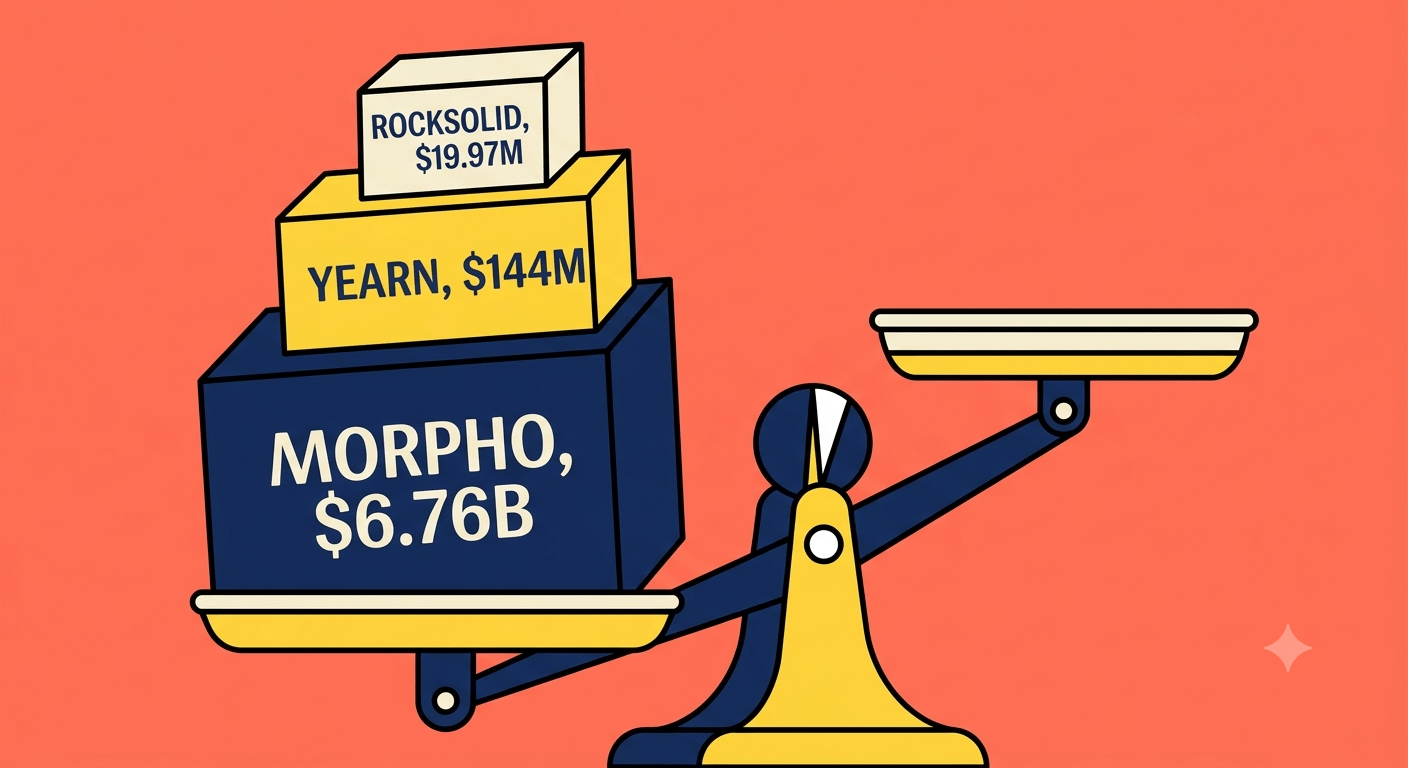

Morpho hit $7.2 billion in total value locked in its lending markets this year, making it the third-largest DeFi protocol by TVL outside of liquid staking. Yearn Finance, the category pioneer, holds $144 million after surviving four years of yield compression, governance chaos, and a market that moved past its original thesis. And then there is RockSolid Network, the 18-month-old vault platform that raised $2.8 million from Castle Island Ventures last year, holds $20 million in deposits, and has zero name recognition outside Rocket Pool's existing community. Three protocols, three wildly different TVL numbers, one market.

The pattern is this: the Ethereum vault market is sorting into three distinct clusters (infrastructure, aggregation, and curation) and the capital is concentrated at the extremes. RockSolid occupies the awkward middle position where it is neither big enough to be the default nor differentiated enough to be irreplaceable. And that gap is not just a TVL problem. It reveals something about what vault users actually want, and it is not what RockSolid is selling.

The three clusters of the DeFi vault market

The Keyrock report on automated yield vaults from June 2026 puts the total market at $18 billion in assets under management. Within that, three distinct models have emerged.

Morpho ($6.76B) is infrastructure. It provides permissionless lending markets that vault curators (Gauntlet, RE7, institutional teams) configure with specific risk parameters. Morpho does not decide where your money goes. It provides the rails for someone else to decide. Users do not deposit into "a Morpho vault." They deposit into a Gauntlet-curated USDC vault that happens to run on Morpho Blue. The brand is invisible. The curatorship is the product.

Yearn ($144M) is the aggregator. It accepts deposits and deploys them across multiple yield sources, rebalancing automatically as rates shift. Yearn's v3 architecture lets multiple strategies compose inside one vault. The pitch is "deposit once, earn the best available yield, don't think about it." It was the dominant model in 2020 and the model that still defines how most people think of DeFi vaults, even though the capital has moved elsewhere.

RockSolid ($19.97M) is the curator. It takes deposits in one asset (rETH), deploys them into one protocol (Rocket Pool), and takes a 1% AUM fee plus 10% of rewards for the simplicity. There is no strategy rebalancing, no multi-protocol allocation, no curator rotation. The pitch is "this vault does one thing, does it well, and will never change." It is the most opinionated of the three models and by far the smallest.

What the capital flows tell you

The $6.76B in Morpho did not materialise because users wanted better lending rates. It appeared because institutional allocators (the wallets holding over $1 million that the Keyrock report says supply 70-99% of vault AUM) wanted legible risk. A Morpho Blue vault has a named curator, a disclosed risk methodology, specific markets it allocates to, and a predictable APY band (4-8% on USDC). BlockEden.xyz put it plainly in its May 2026 analysis: "The pitch isn't 'we'll find you the best yield across 800 options.' It's 'Gauntlet curates this vault, here is the risk methodology, here are the markets it allocates to, here is a 4-8% APY on USDC.'"

Yearn's $144M tells a different story. It is the legacy of the 2020 aggregation thesis (deposit once, earn maximally, trust the strategist), but the capital that once filled Yearn's vaults has been steadily migrating to curated vaults since 2024. Yearn's v3 pivot to modular, strategist-managed vaults is its own admission that the pure-aggregator model has a ceiling.

RockSolid's $19.97M is the hardest number to read. The protocol launched at approximately $20.7 million in November 2025, grew to $29.6 million in April 2026, and is now back to $19.97 million. On a launch-to-current basis, the TVL is unchanged. The peak was a modest bump that reverted. The question is not why TVL declined. The question is why, with zero losses during three market crises and a blue-chip investor like Nic Carter, the number has not grown.

Co-founder Steve Pack described the team's approach to the Metaverse Post in October 2025: "Short-term yields aren't bad if they're based on solid fundamentals. But if the yield is high because the team isn't doxed or the reputation is questionable, we avoid it." That is honest and defensible. It is also the same positioning that keeps RockSolid's APR at approximately 7% (barely 3-4 percentage points above base Rocket Pool staking), which is not enough premium to pull capital out of a Morpho Blue USDC vault or a Yearn multi-strategy position.

The competition RockSolid does not name

RockSolid's official website leads with "institutional-grade liquid vaults" and white-label B2B builds. The consumer rETH vault is listed as an implementation, not the product. That framing signals where the team believes the real value is: building custom vault infrastructure for protocols, custodians, and treasuries.

The problem is that every dollar in TVL is in the consumer rETH vault. The B2B pipeline (the custom MPC vaults, the partner integrations, the institutional deals that justify the $2.8 million Castle Island pre-seed) has not shown up in the numbers. The team may have deals in the pipeline. But in a market where Morpho attracted Société Générale and Bitwise as depositors, and where institutional allocators are actively deploying into curated vault structures, the absence of any institutional TVL on RockSolid's books is a signal that the B2B story is further out than the homepage implies.

Nic Carter, whose firm Castle Island Ventures led the pre-seed, described the vision to The Block: "They are not building another experimental protocol. They are creating vaults that make it easy for anyone, from institutions to communities, to access DeFi strategies without the friction." That is a clear bet on curation over aggregation. But curation as a product category requires something RockSolid has not yet built: a reputation durable enough that depositors choose the vault because of the curator, not because of the yield.

The awkward middle

The vault market has answered a question that RockSolid's founders may not have asked explicitly: institutional capital wants legible risk from named curators, and Morpho's structure delivers that better. Retail capital wants the best available yield from a trusted brand, and Yearn's history still holds that position. RockSolid sits between them: too curated to attract the yield-chasers, too small to attract the institutional mandate capital, too single-protocol to offer the diversification that curated vaults on Morpho Blue provide.

None of this means RockSolid is doing anything wrong. The team is executing on a clear vision: single-protocol alignment with Rocket Pool, controlled growth, conservative strategy. Pack also told the Metaverse Post that "some strategies work beautifully at $10 million TVL but not at $100 million" (an honest acknowledgement that the protocol is building for its current size, not trying to fake scale).

But the uncomfortable truth is that RockSolid's current position ($20 million, flat TVL, 7% APR, single protocol) is a retention position dressed in growth language. The depositors are there because they trust the vault, not because they are excited about it. And trust alone does not compound.

What the positioning spectrum means for founders

The lesson here is what happens when a market stratifies into clear tiers and your product fits cleanly into none of them.

Infrastructure wins on composability and network effects: the more teams build on Morpho, the harder it is to leave. Aggregation wins on brand and history: Yearn's name still means something to the institutional allocators who survived the last cycle. Curation wins on curator reputation: the vault is only as trusted as the person who manages it.

RockSolid has the curator model but has not yet built the curator reputation. It is betting that "first official rETH vault" and "Rocket Pool alignment" are sufficient differentiators. They may be, if Rocket Pool's share of ETH staking grows from its current ~3-4% to something that makes RockSolid the default vault for rETH holders. But that is a bet on someone else's trajectory, and the timeline is not RockSolid's to control.

The 220+ depositors who have placed 5,300+ rETH in RockSolid's vault have made their choice. The question is whether the next 220 will find a reason to, and whether the current ones will stay when the APR dips another percentage point and the spread over base Rocket Pool staking becomes too thin to justify the vault fee.

Lauren Mae is a fractional marketing lead for teams building complex products. She writes about the strategy gaps between what a product does and how it is understood. You can read more about her approach on her services page.